CHINA’S PORK SUPPLY CHAIN IN THE SPOTLIGHT

The rapid evolution and development of that part of the pig meat sector, and the sheer size of China’s pig and pork sector, means that regular updates and reviews are necessary. In this second article in a series, here is a closer look at China’s pork processors.

In the first article in this three-step series, one aspect of the changing face of China’s pork sector was the drive by Beijing to attract large integrated pig production to the north east of China. That brings pig production closer to China’s major grain producing area. Eight major companies are reported to have expansion plans to produce (altogether) around 17 million pigs annually in the north east and pig numbers in that region of China are expected to double to around 120 million pigs a year. That’s about a fifth of China’s annual output.

On the face of it this seems to be a logical rationalisation and restructure for the supply side – especially as many smaller pig producers and processors in China have been ‘discouraged’ by the introduction of stricter environmental regulations. On the demand side statistics on the throughput of pig meat in ‘wet markets’ are not easy to find but there is anecdotal evidence that the trend is negative. Certainly, younger, newly urbanised Chinese consumers are using their spending power in modern shopping malls, supermarkets and convenience stores and are a market for semi-processed and processed pig meat products. This change in purchasing behaviour will work against wet markets and the relatively simple supply chains associated with them. Hence, we see restructuring of supply and demand for pork in China.

A rapidly disappearing sight in China? Pork sales at the road side in downtown Chongqing. Photo: Vincent ter Beek

Moving up the value-added chain

Changes in consumer behaviour will also spur Chinese pork companies to move up the value-added chain and offer more semi-processed products. Other factors that work against wet markets include food safety issues (worries about the spread of Asian flu-type viruses) and (crucially for some wet markets) the soaring development value of market sites in urban areas. As ever, residential housing values affect the location of commercial premises.

But if the demand side looks hopeful for owners and investors in a modern processing sector in China, there have been reports that indicate that some Chinese pork companies are having difficulties. Capacity issues are one aspect – with persistent hints by some analysts and in some company reports that too much investment may have been made too quickly (over capacity and underutilisation).

Reuters reports that around 70 billion yuan (US$ 10.94 billion) in new farm investment has been announced by 26 listed companies since 2016. Companies like CofCo, Wens Foodstuff Group and the WH Group, have ramped up investment in production and processing in recent years, leading to overcapacity.

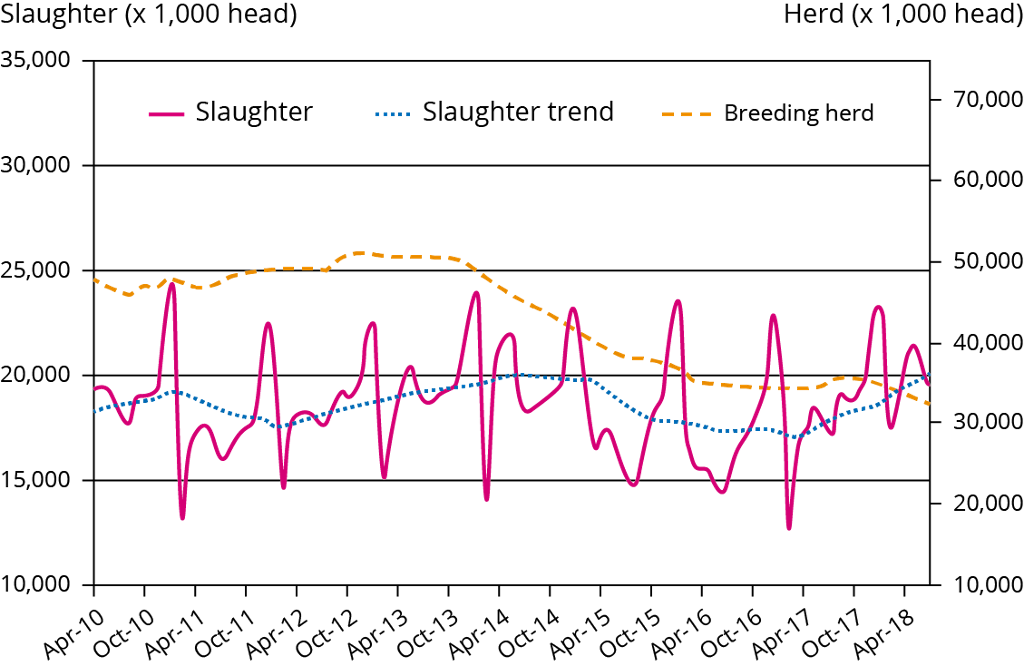

Figure 1 – Chinese hog slaughter and breeding herd, April 2010-June 2018.

Lifting the pork output

Wens, which produced 17 million pigs in 2017, is aiming to lift output to 27.5 million hogs in two years. The latest slaughter numbers for China as a whole show that kill numbers have been growing at very high monthly rates in 2018. Clearly, there has been no shortage of money for these investments; the Agricultural Development Bank of China is reported to have agreed a credit line of at least three trillion yuan ($ 450 billion) by 2020 for the modernisation of China’s agriculture industry.

A different kind of capacity issue is ‘know-how’, i.e. the time needed to acquire and apply technical knowledge in a commercial environment. For China’s processors this is ‘the’ challenge. Meat processing technology and the managerial ability and workforce skills to handle its associated equipment and processes, need investments in training (personnel, time and practice) to enable know-how to be used effectively.

Whilst domestic pork companies rush to make these investments, they will see some competition from foreign players – Danish Crown and Hormel have announced plans to invest in factory facilities in China to manufacture the processed products that younger Chinese consumers are demanding. Cool chain logistics and presentation in store also need parallel investment by distributors and retailers – so, unless they are totally integrated, pork companies face another supply hurdle there. Big data, digital business models and e-commerce are also features of Chinese pork companies’ investments. It’s not just all about the cutting and packing plants and this all adds up to a vibrant and potentially disruptive landscape for the supply side.

Table 1 – Growth in Chinese hog slaughter.

By Pig Progress

Partnering with other firms

One way of dealing with the know-how issue is to partner with domestic or foreign firms that have expertise in the needed skills. This has been happening in China. Some recent examples of Chinese pork companies seeking to improve their supply chains and processed product ranges include the recent link up between New Hope Liuhe and the French pork processor Cooperl Arc Atlantique. They have signed a strategic cooperation agreement and the two sides will work together to build a complete pork industry chain in China, producing high-quality pork in China in five to ten years.

In a separate development, the website Meicai has become China’s largest fresh B2B e-commerce platform and New Hope Liuhe will cooperate with Meicai to create new modes and e-commerce opportunities. Yet another example is the link between Guangdong Wens Food Group and NetEase’s cloud computing and big data brand Netease. Wens and Netease have agreed a strategic cooperation, relying on the advantages of Wens position in animal nutrition and food processing and the expertise of Netease in cloud computing, big data, artificial intelligence and e-commerce.

The descriptions and reports in the preceding paragraphs illustrate how the Chinese pork and pig meat sector is under pressure to deliver more, change rapidly, and become more efficient and customer-led. The large Chinese pork companies are mostly integrated and have links down and up the supply chain but we will see more cross linkages across sectors in the future. It’s an old saying in China and relevant here, Chinese pork processors are living in interesting times.

Dr John Strak

Editor Whole Hog | www.porkinfo.com

Source: www.pigprogress.net